I routinely hear the question: Is Title Insurance worth it?. My answer, is yes, it is quite important. You wouldn’t buy a house without homeowners’ insurance or buy a car without car insurance. I’m sure you have Health and Life insurance. If you are protected in other aspects of life, why would you not protect the title to your home as well? and does not have liens attached? The best part is that title insurance is a one-time fee that is paid at closing and you never have to worry about it again. As long as you own the property it is protected. So it would be crazy not to do it!

Who thought up Title Insurance… and why?

Title Insurance used to be done by opinions given by Conveyancers prior to 1876 when Joshua Morris founded Real Estate Title Insurance Company of Philadelphia. The purpose was to have land conveyances financially guaranteed instead of the old system of relying on opinion-based reporting without financial backing. Now, instead of “trust me” the industry offered “if we are wrong, I will pay you.” Other companies in Chicago, Los Angeles, Minneapolis and New York followed shortly after and ALTA was created to assist in standardizing and unifying the Title Insurance industry.

What is ALTA?

In 1907 the American Land Title Association (ALTA) formed as the primary association of the Title Insurance industry. The association set the precedence for title insurance, they did not standardize title insurance policies nationally until 1929.

What can Title Insurance protect against?

Title insurance protects against hidden issues, liens and encumbrances that can be costly to the new homeowner. The following are examples of potential issues:

Lack of Access

Unpaid Mortgage

Seller claims to have ownership, but do they really?

Neighbors have an easement through the property

Previous owners deceased family member is buried on the property

Legal Judgment for previous owner that attached to the property

No one is exempt from uncleared title issues. Even Abraham Lincoln’s father lost his home to title defects when Abe was a little boy…Twice.

So, why title insurance?

No one wants to live with the fear of losing their home due to a claim by someone else or from a lien that could put their home in foreclosure. Especially if they the option to have an insurance policy that says they own their home and no one else has a claim to it. Title Insurance, while not required, is still very important.

Title Insurance can sometimes be overwhelming and appear confusing. However, the Tallgrass Title team is here to assist with your title insurance questions, just give us a call!

Real estate fraud is alive and well as fraudsters find new ways to cheat people out of their money. Whether it be through fraudulent emails or posing as a realtor and calling clients to get them to send money. Title companies, banks and realtors strive to protect buyers’ and sellers’ money as if it was their own money. It is our job to protect our clients and ensure a smooth closing process for everyone. We were asked recently what we do to protect our clients’ sensitive information and protect their assets. We take this very seriously and want to share a few ways we do this.

ID Verification

When Sellers come to our office to sign documents to sell real estate, we check photo identification. We ensure the party “selling” is in fact the party in title and not a fraudster claiming real estate as their own.

Remote Online Notarization (RON)

Believe it or not, signing documents through a RON environment is more secure than signing in person. Signers must submit their photo ID while on a live audio-visual session, like in person. But they also answer KBA (Knowledge-based authentication) questions to verify their identity. We simply do not have that kind of capability in person and this adds an extra layer of identity verification.

Secure Wire Instructions

We work with CertifID to send and verify wire instructions. It takes a little extra time to verify your identity and banking information with this process. However, we do this to guarantee funds are getting to where they are supposed to be instead of being sent to a fraudsters personal account.

Earnnest

“You spelled that wrong.”

We hear this a lot, however, I assure you we know how to spell. Earnnest is a payment portal we use to request earnest money from our clients to satisfy the terms of the contract. It works a lot like Cash App or Venmo, is secure, and the Earnest Money goes straight from the buyers bank account to ours. We simply send your buyer a link to our custom payment portal and they complete payment. This reduces the need to navigate wire instructions and the possibility for human error. There is also a cost savings over cost of sending a wire, in most cases.

E-Signature Platforms

Our office utilizes Dotloop and HelloSign to get documents to clients securely. We can send view only documents or we can send documents with a request for information and signatures. This eliminates the requirement for password protecting a PDF in email and still applies the security necessary to protect sensitive information.

Password Protected

If our office does send out sensitive information via email, we will always password protect it to secure information that is not public knowledge, such as settlement statements. At any time, a fraudster could be hanging out in your email and open attachments that are not secured to see what the proceeds would be for a transaction, then reach out to you with bad wire instructions requesting you send your hard-earned money to then instead of to the title company for your transaction.

Why?

Wire fraud and other forms of cybercrime in the real estate sector resulted in $350 million in losses in 2021, up from $213 million in 2020. While only 12,000 people a year are victims, one in three real estate transactions is a target. This is why we remain vigilant in our own practices and in our efforts to educate our clients.[1]

A staggering 35% of fraud attempts reported in 2021 were traced back to email. If you suspect a fraudulent email was sent to you, do not respond to it, click any links, or open its attachments. Reach out to your realtor, title company, lender, client using known information from a source outside of the email. Stay tuned for a follow-up blog on email security tips!

We are here to answer any questions you may have, protect your information, and help make your closing experience as smooth as possible.

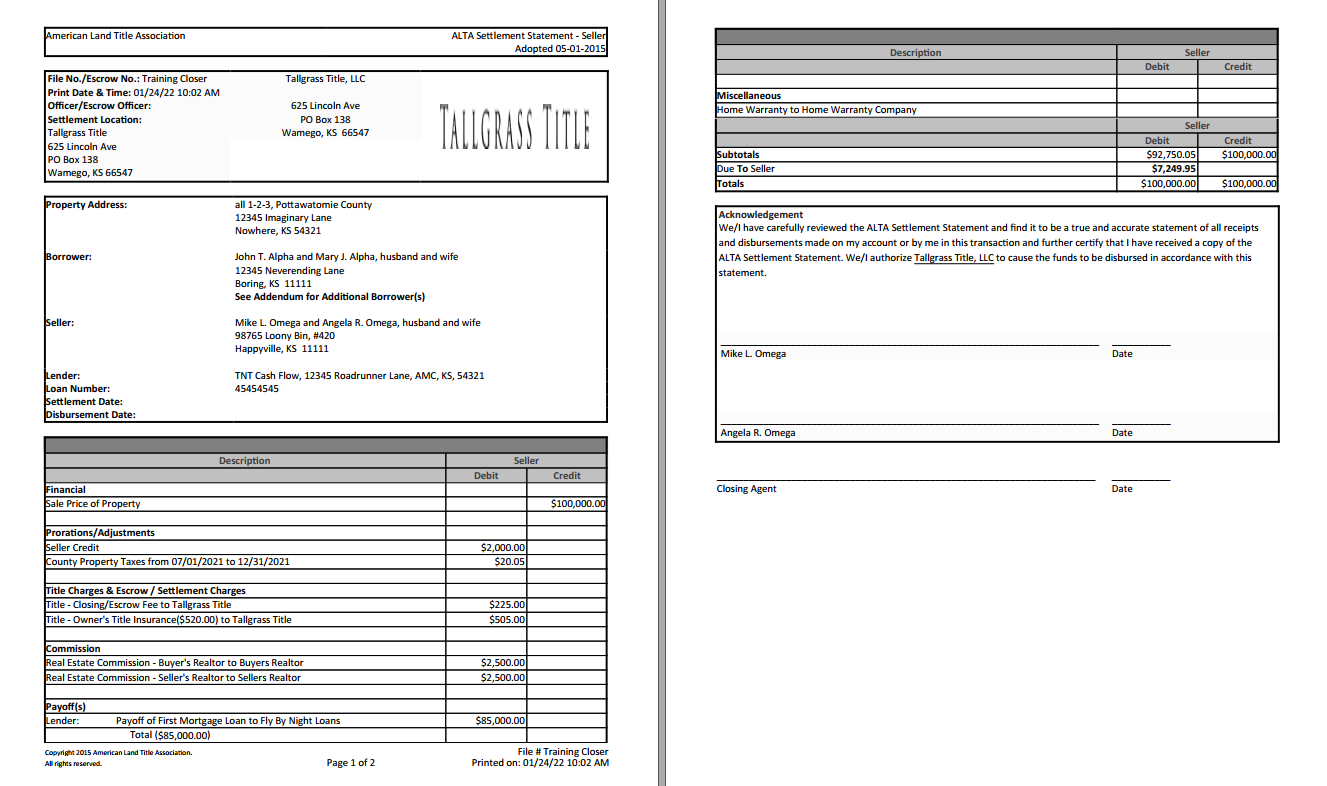

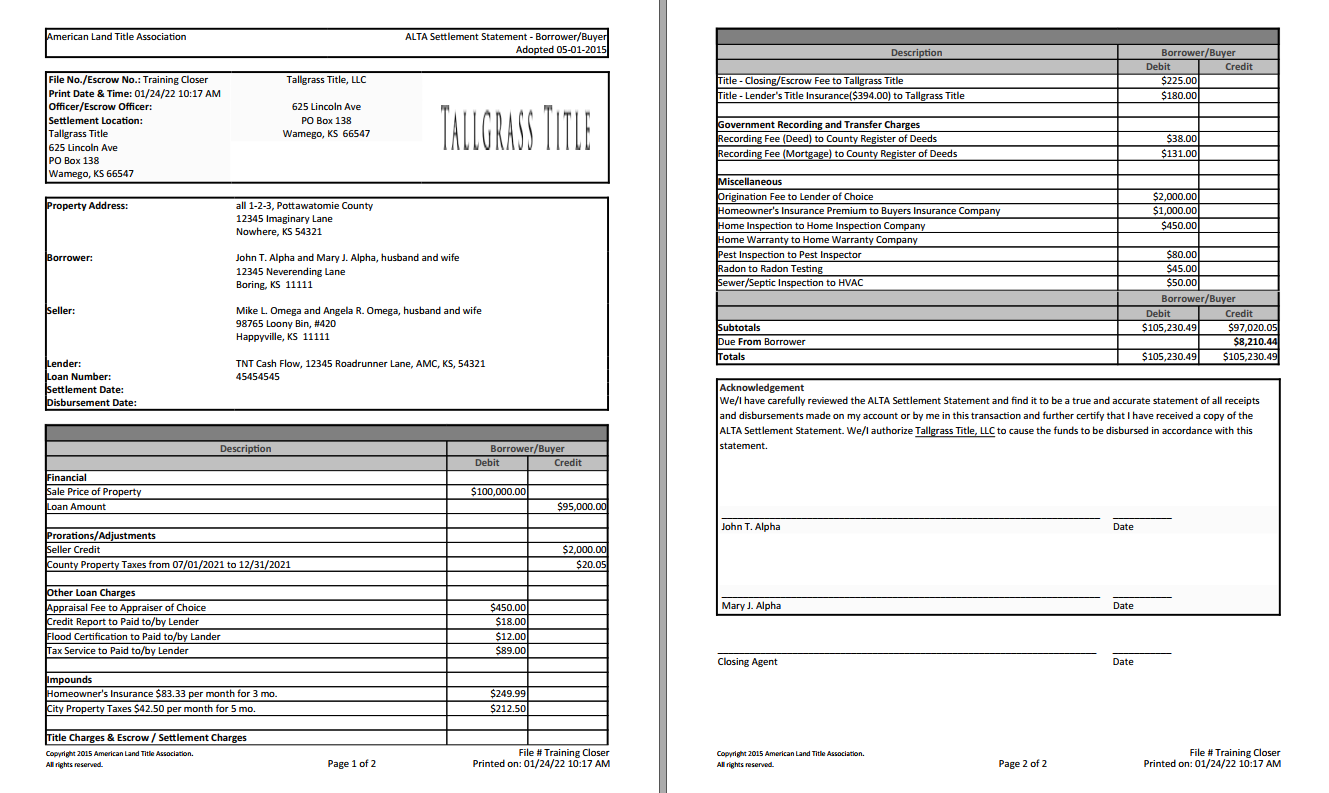

As we prepare to close a transaction, we create settlement statements, which are documents demonstrating all debits and credits associated with the transaction. The American Land Title Association (ALTA) has provided a standard template for these forms, so they are recognizable and readable, no matter which title company you close your next transaction with. Whether the transaction is cash or financed, our office will provide ALTA Settlement Statements to both the Buyer and Seller. The Buyer and Seller statements are unique to their respective side of the closing and can only be shared with the other party if we have express permission in writing.

Sellers

When reviewing the Seller Settlement Statement you will find the sales price, any applicable credits the Seller gave to the Buyer in the contract, a tax proration (either a credit or debit depending on the time of year and if Seller paid them prior to closing or not), title expenses that consist of closing fees and title insurance premiums owed to the title company, any commissions due to realtors, payoffs of current liens, and any invoices or repairs that the Seller has agreed to pay for.

Buyers

When reviewing the Buyer Settlement Statement you will find the sales price, any applicable loan amounts, any applicable Seller credits the Seller agreed to within the contract, a tax proration (either a credit or debit depending on the time of year and if Seller paid them prior to closing or not), loan closing charges determined by the lender, impounds for the Buyers new escrow account collected at closing by the lender, title expenses that consist of closing fees and title insurance premiums owed to the title company, recording fees to file the deed and mortgage of public record with the county register of deeds office, and fees for any inspections or additional work the Buyer has requested prior to closing.

Buyer Settlement Statements may also be referred to as Buyer Settlement Statements.

Bottom Line

Both the Buyer and Sellers statements will include an amount that is either due from or due to that party. If an amount is due from, this represents the amount due to the title company to close the transaction. If an amount is due to, then you should expect a proceeds check following closing!

This Buyer/Borrower settlement statement reflects the amount the due from the borrower in order to finalize the transaction.This Seller settlement statement reflects the proceeds the seller will receive after all seller costs are paid.

Signing

As part of “closing” Buyers and Sellers need to review and sign their respective ALTA settlement statements in order to acknowledge their acceptance of the breakdown of debits, credits, and bottom line.

Sellers are more than welcome to sign in our office, with their realtor, on their own or electronically.

Buyers of cash purchases can do the same as above but in the case of a loan will need to sign with the title company, lender or mobile notary.

Questions?

If you have questions about you or your client’s ALTA Settlement Statement, give us a call! We are here to help make this a positive experience.

Closings with Karissa is back with a few helpful reminders on property taxes and second half payments.

It’s that time of year again.

Real estate taxes are due to the county treasurer. Do you pay them before closing? Will the Title Company pay them before closing? What if the seller’s lender pays them before closing and the Title Company collects for them too? These are some of many questions that might swirl around homeowners’ heads right before closing.

First & Second Half

Taxes are available for payment in November of the current year with due dates of December 20th of the current year and the following May 10th. Taxes can paid in full in December or paid half and half in December and May. They first half is considered delinquent on December 21st and will start accruing late fees and penalties on that date. The second half is considered late on May 11th and will start accruing late fees and penalties on that date. If your closing is taking place after one of those dates and you do not have taxes set up in escrow, it is advisable for payments to be made prior to closing to avoid extra charges.

Taxes & Your Closing

Taxes are considered a lien on real estate. They are always there (unless the landowner is tax exempt) and will be in first lien position to all other liens – including mortgages. This means that taxes will always be paid out first in the event of a court action and your closing agent will make sure that tax payments are up to date. If current taxes are not yet paid, they will apply that payment to your settlement statement to be paid at closing, including any applicable fees.

If closing takes place in October or November, it is likely that the seller rather than the buyer will receive the annual tax statement. This is because the county treasurer’s office may not have new owner information updated prior to mailing out November tax statements. If this happens the taxes are still the responsibility of the party that agreed to pay the year’s taxes as part of the real estate contract.

Things to remember:

Taxes are due December 20th and May 10th

The Title Company will pay off taxes based on the terms of the contract

The Title Company will never keep funds collected for taxes already paid, they will always refund payments rejected by the treasurer for previous payment.

If you have more questions about taxes, please reach out to your closing agent and they will walk you through taxes and prorations. It is our job and our pleasure at Tallgrass Title!

The heart of any real estate transaction is the contract. It is the meat and potatoes. Everything that the realtors, lenders and title company need to know to close a deal is in the contract and any amendments or addendums that follow.

Therefore, it is important to have everything that the parties desire within the transaction clearly outlined in the contract . This might include a seller credit or home warranty, Or if certain appliances are to stay or go with the seller. All these things must be included in the contract to set a standard of expectation. It also prevents incidences of: “Well that was my washer and dryer” and the seller running off with appliances the buyer is expecting. Or even worse: “That other lot was supposed to be included.” If it wasn’t on the contract, it won’t get conveyed.

Here are some helpful tips to make sure there are little to no issues when writing your real estate contract:

Identify the Real Estate

Know what you are selling. Even if all you have is an aerial from Google Maps with a hand drawn outline of what is intended to be sold and an address. Send that to your title company and ask for a preliminary report. In their search process, they will the correct legal description to include on your contract, preventing issues later with lots or tracts being omitted or included by mistake.

Identify the Parties

A preliminary report will include how the real estate is currently vested. So, if John and Jane Smith want to sell their house, the preliminary report will note that the property is actually owned by John A. Smith and Janice Smith (their legal names) or Jane Smith’s Trust.

The Buyer in the transaction will direct how they want to take title to the real estate on the contract. The buyer might prefer to take title with first, middle and last names or just first and last. Or they may request to take title via a trust or a company. This should all be included on the initial contract or a follow up Addendum.

Set a Purchase Price and Terms

Agree on a purchase price. Once the purchase price is decided, set the terms. Who will pay closing costs to the title company, title insurance and any? Will there be a Home Warranty and who will pay that and how much? Is the Seller willing to offer a seller credit to help with the buyers closing costs? What stays and what doesn’t stay with the property? Never assume that appliances stay, even if it seems logical.

Pick a date to close

Closing dates can be very flexible and easily changed with addendums so long as all parties agree to it. Often contracts will state “on or before” and that just means that at any time before the stated close date in the contract the transaction can be closed if all parties agree. In the current market, unless it is a cash deal, give yourself, your client, and lender time and set closing out 30 to 45 days. Best practice is to avoid closing on the very first or last day of the month as these are the busiest days for closings, and it may be difficult to get the time you want unless you schedule early.

Ask questions

If something doesn’t seem right to you, ask questions! For Buyers purchasing or sellers selling a home this is a huge change and can be very tense. We understand the stress of each transaction and are here to help and answer any questions. Even if they seem trivial, we are happy to assist and walk you through the process, it’s our job!

We have a saying in our office: “early deed packets means smooth closings!” But why would a few signed documents mean closing would run smoother? The more information we receive ahead of closing allows our closing team to gather any additional information we may need well in advance. An early and complete deed packet allows us to balance with your client’s lender and get final numbers out for buyers in cash transactions. That way, when the day of closing comes around finalizing the transaction is a smooth process, leaving more time for celebration and little to no concern about whether things will fall into place.

Deed Packets contain several documents that consolidate much of the information we will need prior to closing. This includes a form that allows us to contact the Seller’s current mortgage holder to obtain a payoff. This is especially important right now with many mortgage companies experiencing staffing shortages with extended processing times. Oftentimes, it can take up to 20 days to get payoffs returned to us.

Early deed packets also allow us to deliver early settlement statements to you and your clients. This gives plenty time for review and provides a clear picture of what the closing day will look like on the financial end of the transaction.

Additionally, some expenses will not be clear to us until we have the deed packet returned, including information about Homeowners Associations. Having information about a property’s HOA membership in advance allows us to ensure that prorations are applied appropriately at closing.

This early document package also contains important information about email fraud and wire fraud. We want to help protect your client’s money just as much as you do. This information is available to all of our clients in order to inform them of the dangers of spam emails and the possibility of fraudsters intercepting wires. Likewise, we include information about how we protect our clients from theft with CertifID. We use CertifID to send or verify wiring instructions prior to the day of closing.

We understand sometimes coordinating a deed packet signing can be an issue as schedules vary. Your clients are more than welcome to come to either of our offices Monday through Friday during business hours and we would be happy to walk through the deed packet with them. Alternatively, we offer free courier service and would be happy to meet your clients at a convenient location in Manhattan, Wamego, Alma, and Westmoreland.

Should you have any questions about the contents of a deed packet, feel free to contact one of our real estate professionals to assist you through the process. It’s our pleasure to assist you!

In today’s market with interest rates so low everyone is looking to buy. Why is it important to pick the right closing day? What are the best and worst days to close? For most clients, the bottom line is “When will my proceeds check be ready?” or “When may I move into my new house?”

Any day is the best day to close! You are purchasing a home and are anxious to move in or are ready to close on the sale of your home and eager to use the proceeds for another transaction. However, based upon the hectic housing market and record transactions taking place, certain days may just not be as convenient for all parties as others.

We will start with the best days to sign. From a title and lender standpoint the best days are Tuesday through Thursday with the exception of the 1st, 15th, or last day of the month. No one really wants to leave work early, come in late or take a day off in the middle of the week to go sign a bunch of papers, right? But those are the least busy days for a title office or lender which for the client means more flexibility on scheduling the appointment, more time available to go over specific questions about the transaction, and a more relaxed atmosphere.

So why are certain days less ideal than others? The short answer is that Fridays just seem to be a popular day for closings. We are also seeing an increased volume of closings on Mondays as well as the 1st, 15th, and last day of the month. While closing can still take place those days, scheduling will not be as flexible, and the appointment may be restricted to a certain time frame due to the high volume of other transactions.

Another consideration to make is that picking a Friday to close could actually result in further delaying your transaction if something doesn’t go as planned or a funding number is not received by the close of business. If a Friday closing has to be delayed for whatever reason, the earliest it can occur would be the following Monday or even Tuesday if the issue that caused the delay cannot be corrected in enough time for a Monday closing. If Friday is your only option for closing, consider closing in the morning to ensure funding can take place before the end of the business day.

So when will the checks be ready? Most lenders have requirements to be met before authorizing the title company to fund each transaction. This can take anywhere from a few minutes to several hours. Rest assured that as soon as funding is authorized, we will issue checks and notify all parties.

For updates on your transaction, we offer Ready2Close. This portal allows clients to track the progress of their closing with a milestone tracker. Clients can also securely transmit and receive documents, e-sign certain documents, and access contact information for those involved with their transaction.

Getting Deed Packets signed early is an essential part of the closing process. It helps your Closer calculate certain fees, pull payoffs if there are any, and makes it possible to verify information for post-closing tasks well in advance

There are quite a few documents in every deed packet and it might be difficult to remember what they all mean if your client asks, so today I will walk through our Deed Packets and what each document is used for. As always, our team remains available to answer questions that you or your client might have about completing these documents. So don’t hesitate to give us a call!

Fraud Warning Fact Sheet

We use this form to make our clients aware of wire fraud and our partnership with CertifID to ensure that all wire instructions are verified and insured when the funds leave our office via wire transfer. Each statement will need to be read and initialed and then signed at the bottom.

Authorization for Release of Information (Payoff Requests)

This form allows us to request payoffs for existing mortgages in order to clear them at closing. The more information provided, the easier it is for the closing agent to obtain the payoff. Along with the signature line is a place to include the Sellers SSN and the date they signed the release.

1099 Tax Information Sheet

The top portion of this form will need to be filled out completely with the Seller’s Address, Phone number, and SSN or EIN. This will help us send out accurate 1099s the following January.

Proceeds Instruction Sheet

These are instructions for us to disburse the proceeds and how to get them to the Seller in the transaction. Once a selection has been made from the list we will need the form signed and returned with the rest of the packet. These instructions can always be changed by signing a new form with new instructions.

Authorization to Pay Commission

If there is a realtor, this one allows us to get the realtor paid at closing in the accurate commission amount as designated by the Agreement. It will need to be filled out whether there is a commission percentage or flat fee. If there is a Seller Realtor Admin fee, there is a place to include that as well and then it will be signed by both Seller and Listing Agent.

Homeowners Information Sheet

Not all packets will include this form. If the real estate is not located in a subdivision or we know that there are no HOAs in a certain subdivision, we will not include this. If it is in the packet, we will need to know if there are HOAs. If there are not, the “No” box will be checked and you can move to the next form. If there are HOAs then the “Yes” box will be checked; please complete as much of the HOA contact information as possible.

Authorization for Release of Information to Designated Realtor

This form will not change how we treat the transaction. Sellers have the option to direct us not to share their private information with the Buyers Realtor. If the top box is checked, directing us not to share information with anyone other than their realtor or lender, then we cannot and will not share a settlement statement with anyone, even those involved in the transaction, other than their realtor and lender.

NOTE: To prove commissions have been applied appropriately we can send a heavily redacted version of the ALTA settlement statement that only shows commission amounts and the Sellers signatures.

Covid-19 Notice of Possible Delays

This one is a notice that lets everyone know that there could be delays related to Covid-19 with getting documents recorded, back from recording and getting final policies issued.

Notary Instruction, Identification Verification and Notary Information and Certification

When documents are notarized, our office needs proof that the notary checked the identification of the signor and that the notary is in good standing with the state in which they are bonded in. It will also help in the event that we need to contact the notary if we have any questions regarding the notary’s information.

Affidavit as to Debts, Liens and Indemnity

This affidavit is a statement made by the seller that there are no liens or potential liens, or that no one holds an interest in the real estate that we would need to clear up prior to closing. This will need to be signed in front of a notary.

Limited Power of Attorney

We include a Limited Power of Attorney in all of our packets for Sellers to utilize. If signed it allows the realtor to sign settlement statements and any Buyer loan docs on behalf of the Seller. It is not required and is solely at the option of the Seller to sign.

Deed

The Deed varies as much as the transaction itself as to what kind of Deed is used to transfer the real estate. This will need to be signed by everyone who holds an interest in the real estate to complete a free and clear transfer. We hold the deed in our office until the transaction is closed and funds have been disbursed. At that time we record the deed with the county register of deeds to complete the transfer. The original will be sent to the buyer with the final loan policy.

In addition to the above, other documents may appear in a deed packet on a case by case basis.

Affidavit of Non-Production – Used to clear existing expired oil and gas liens.

Affidavit of Child Support or Spousal Maintenance – Used to clear divorce/child support cases.

Certificate of Trust – Used to prove the trustee signing has authority to sign.

Corporate Resolution – Used to prove the signor of a company has authority to sign on behalf of the company.

Affidavit of Death – Takes the place of a death certificate to clear title.

The earlier in the process we can get these documents signed and back to our office, the smoother we can make the whole closing process. Everyone in our office is a notary and we are more than happy to meet with clients to get Deed Packets signed.

We do offer a free courier service and can send someone to you to get everything signed if you just can’t get away. Just call our office and set an appointment for a time that works best for you.

It’s property tax season! In Kansas, property taxes are due in arrears and paid twice a year. Taxes for the first half of the year are due December 20th of the current year; the second half of the year is due on May 10th of the following year. This means that unpaid taxes for the current year are considered delinquent as early as December 21st.

In order to avoid delinquency, we recommend paying before December 20th, otherwise you could encounter long lines or delays in processing your payment. With varying restrictions due to Covid-19, be sure to contact your county treasurer in advance to see if an appointment is required to pay your bill or be sure to mail in your payment early enough to ensure it is postmarked prior to the due date.

Selling your real estate?

If your real estate is currently under contract, you may have very specific questions. Like, what if I am selling my real estate and the closing date is near the tax due date? How does our title company handle taxes? Do we pay them ourselves? Do we pay them at closing?

First, take a deep breathe. Then call your closing agent and ask them how they would prefer to handle the taxes.

If the closing date is prior to the due date your closing agent may prefer that you wait and pay the taxes through closing. If they are due after closing, they may encourage payment prior to closing to prevent late fees and penalties. Either way, if a payment is made your closing agent will need proof of payment in order to remove the payment from the settlement statement. Otherwise funds will be held in escrow and paid to the county by December 20th or refunded to the Seller upon proof of payment prior to December 20th.

How do I get proof of payment?

When paying taxes in the county office, the treasurer will provide you with a receipt for your payment. Hand deliver or email a copy to your closing agent and they will take care of the rest. If you mail in your payment, your closing agent can call the county and request the receipt.

If taxes are paid at closing, do I have to take the check to the county treasurer myself?

Nope, the title company will send a courier to the county and take care of getting them paid, you will not need to worry about the taxes getting paid we will take care of everything.

If you are unsure of next steps please feel free to reach out to our office. We can walk you through the process to make your closing as smooth and stress free as possible.

In our current moment of social distancing and increased dependence on technology, many will question what is better: wet ink signatures or electronic signatures. Some may debate that putting a pen to paper and scrawling their signature is a fool proof and tamper proof way to sign a legal document. You may be surprised to hear that electronic signatures through a program designed for just that, signing electronically, are more secure and oftentimes a better way to put your official seal on a document.

How can that be?

You receive an email asking for a signature on a document. You click accept, click to sign, select your signature, then complete the process. How in the world could that be more secure than a wet ink signature?

The programs designed for electronic signings are designed to pull multiple factors of authentication to prove that you are in fact the signer of the document. The records are retained and track the history of actions taken with the document, for example, who opened, viewed, signed and the location each action took place. When the document is completed a certificate of completion is attached to the document showing that all have signed with a time stamp, IP address and any other pertinent information to identify the signer. A digital seal is also attached to that document.

Signing in person is secure as well, however there are not multiple factors of authentication to prove that the signer did sign the document. There is no electronic witness proving the identity, location, or other identifiers provided by e-signing programs, that the signature was put on the paper by the authentic signer.

Both are secure, accepted ways of signing documents in the real estate world. For those who are less electronically inclined, wet ink signatures may be the way to go. For the more tech savvy folks among us, you may prefer clicking a button or using your smart phone to sign documents on the go. Whether you prepare in-person or electronic signings, we are here to help you through the process with helpful tools and friendly staff available to answer questions.