So, you are ready to sell your house: have a buyer lined up, contract signed, and are looking at a prospective closing date. Then you stop and think, “What’s next?”

If you have never purchased or sold a piece of real estate before, or a significant amount of time has passed since the last time you did, the whole closing process can seem a bit overwhelming. In the past, you could just shake hands on a deal and trust that the other party would work with you to get the deed filed, the money given to the right people, and help iron out any wrinkles that might come up later. However, times have changed, and you can’t implicitly trust that the other party will fulfill his part of the bargain or that either you or he will know exactly what needs to be done to complete the sale. What is needed is a disinterested third party to work with the Seller, Buyer, realtors, and the bank to help each party perform the tasks necessary to complete the transfer of ownership. At Wamego Title, it is our pleasure to work closely with each party to the transaction to ensure that each one knows exactly what is expected of them and when each step should be completed.

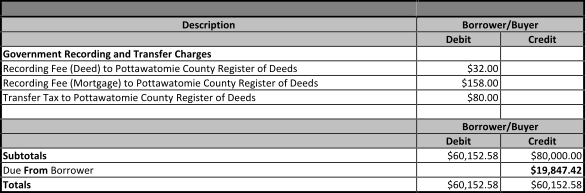

For Sellers, we draft the Deed, Settlement Statement, and any other documents needed to ensure that you are passing clear title to your Buyer. We send the documents to you well before the closing date to ensure that your questions can be answered before closing and leave plenty of time for you to meet with the notary of your choice to complete the necessary documents. If there is a mortgage on the property you are selling, we contact your mortgage holder to obtain the payoff amount and then send the payoff to them during the actual closing. A few days before closing, we will send you, and your realtor if you have hired one, the finalized Settlement Statements so you can review the costs of your transaction before you get to the closing table. At that time, our closing agents will discuss with you whether you prefer to schedule a closing appointment or if a mobile closing would work best for you. During the closing it is our responsibility to receive the secure funds from the Buyer and transfer the proceeds to you.

For Buyers, we work closely with you and your Lender, if you are obtaining financing, to ensure that you are prepared for your purchase. We create your Settlement Statements in collaboration with your Lender prior to closing, so you have time to review it and know exactly what amount of funding you will be required to bring to closing. You and your Lender will be able to decide where it would be convenient to sign your closing paperwork. If you are not using a Lender, we are able to work with you directly to decide what method of closing best fits your busy schedule.

For both Sellers and Buyers, after closing we ensure that all the documents are properly completed and recorded at the County Register of Deeds Office and send each party copies of the documents that should be kept for personal files. Our closing agents are always available to answer questions or address concerns no matter what stage of the transaction you are at!