As most of you know, we recently opened an office in MHK. We had the opportunity to talk a little about our new adventure! Check out the video below!

As most of you know, we recently opened an office in MHK. We had the opportunity to talk a little about our new adventure! Check out the video below!

A few days before your closing, you can expect to receive a document or two called a Settlement Statement and maybe even something called a Closing Disclosure. These documents can look a little intimidating, but we can give you some pointers to help you understand what is going on.

For cash transactions or transactions with in-house financing, you can expect to receive a simplified Buyer’s or Seller’s Statement. This simple statement is set up to be pretty easy to read. Here at Tallgrass Title, we give a separate sheet to the Buyer and a separate one to the Seller to protect your privacy. The fees are set out in a list as shown in the sample Seller’s Statement below:

As you can see, there are two columns showing the debits and credits with the subtotals at the bottom. The last line item is the actual proceeds amount that will be given to the Seller.

If you are purchasing a home and obtaining financing, you may get a loan that will be sold on the secondary market. If you are getting this type of financing, your Lender will give you a document called a Loan Estimate soon after you apply for the loan. Then, during the week before closing, you will receive two final settlement documents. One is called the Closing Disclosure and the other is called the ALTA Settlement Statement. The good news is that these documents will have very similar numbers; the bad news is there are a few more sheets to read through.

The Buyer’s Closing Disclosure is 5+ pages long. Here is a brief overview of what is on each page: 1. Basic details about the type of loan. 2. List of fees associated with the transaction. 3. Credits, subtotals and the grand total of funds you will need to bring to closing. 4 & 5. Further details about your loan and contact information for your Lender, Realtors, and your Title Company. The Seller’s Closing Disclosure is usually 2-3 pages long. Page 1 shows details of the transaction, subtotals and totals. Page 2 lists the fees the Seller has agreed to pay.

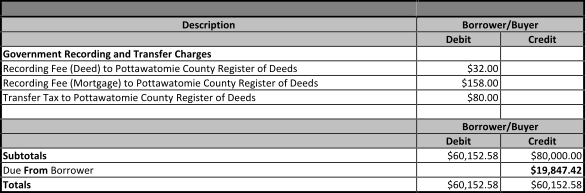

We prepare the ALTA Settlement Statements to go along with the Closing Disclosures. These documents are formatted differently from the simple Statements, but they still show a line-by-line breakdown of the closing fees. Here is a sample of what part of one looks like:

As on the simple version, there is a separate line showing the amount “Due From Borrower”. This is the amount the Buyer will need to bring to closing.

The thing to remember is that you will want to review the documents as soon as possible after receiving them. Don’t wait until the closing to ask your Lender or us any questions that you may have. If you wait until closing to ask your questions it could possibly delay the closing. Please remember that we at Tallgrass Title are always happy to take the time to answer questions and explain information.

As someone who has been interested in buying or selling property you may have heard talk lately about new “TILA/RESPA” or “TRID” rules. So what do these acronyms mean and why are they being talked about by lenders, settlement agents, and realtors, to name a few? Will these rules affect me if I am trying to buy or sell real estate?

TILA and RESPA stand for two different government acts that directed two forms that were provided by lenders to buyers/borrowers during a real estate closing. One act was known as the Truth in Lending Act and the other was the Real Estate Settlement Procedures Act of 1974. There was concern that these two forms were difficult to understand, so in 2010 President Obama signed the Dodd-Frank Act into law. This new law required that the information from the two forms be combined into a standardized Loan Estimate Form and Closing Disclosure Form. Thus, the name TRID came to be: TILA/RESPA Integrated Disclosure.

Lenders are now required to provide a Loan Estimate to any buyer/borrower who is seeking financing for a standard residential home purchase. The fee and term names are used on a similar Closing Disclosure form (instead of the old HUD or Settlement Statements) during closing, so the buyer/borrower should understand more easily the costs of the entire transaction. The Closing Disclosure form also has to be delivered to the buyer/borrower three business days prior to closing so they have a chance to review it and ask questions before they reach the closing table. Prior to closing, the settlement agent will also provide a Settlement Statement that will be signed during closing.

As a Seller, the new rules can affect you as well. For instance, it might take a bit more time than before in order for the bank to gain the proper approval for the loan and be ready to close it. The Seller also is provided a shorter, more compact Closing Disclosure form. Though the three-day delivery rule does not apply for seller’s documents, settlement agents will try to deliver the Closing Disclosure and Settlement Statement a few days before closing so there is time for you to review them.

In conclusion, as either party in a real estate transaction, these new rules will affect you, but if you bring your questions or concerns to Lenders, settlement agents, and realtors, they will work together to provide you with the answers and assistance you need through the entire process.